Insights

Real Estate Development in 2025: Supply Chain Reconfiguration

May 19, 2025

Introduction

Monumental changes are unfolding across global supply chains as the U.S. undertakes an unprecedented shift away from decades of pro-trade policy. We previously articulated a relatively sanguine view of these developments, tying the incoming administration’s trade agenda to a broader, long-term realignment. That view remains largely intact. But with the effective U.S. tariff rate now at 17.8%, the implications have taken on more urgency. This is a volatile, transitional period. Rather than draw premature conclusions, we offer a structured assessment of what long-term equilibrium might look like—grounded in the structural drivers of supply chains and logistics demand.

Structural Shifts Driving Supply Chain Realignment

Our Core Premise

U.S. trade policy, while unusually disruptive in scope, reflects the most acute expression to date of long-running structural trends—including the pursuit of nearshoring, supply chain redundancy, and domestic (advanced) manufacturing capacity. If the current volatility accelerates a shift toward more diversified, resilient, and regionally distributed supply chains—then the long-term impact on U.S. logistics demand is likely to be structurally positive. A more geographically redundant supply chain, one that favors regional distribution networks and manufacturing-adjacent logistics hubs, requires more—not less—physical infrastructure to support it.Nearshoring

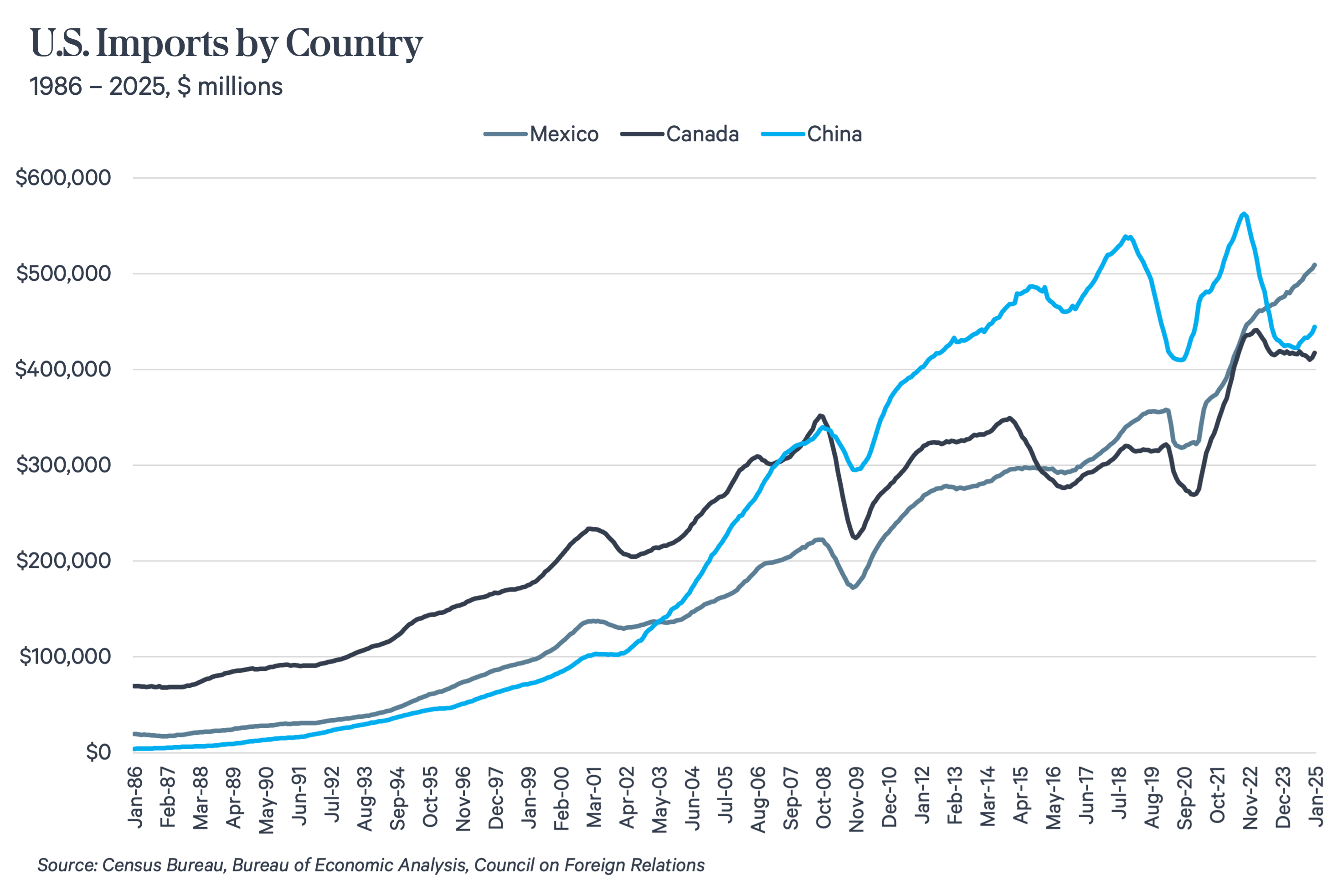

Nearshoring is not just shifting supply chains–it is expanding and reshaping the physical logistics landscape across key U.S. and border markets. For more than a decade, rising costs in several Asian countries, increasing transportation risks, and the inherent advantages of proximity to end markets have steadily pushed North American manufacturing and assembly closer to U.S. consumers. The growing share of imports from Mexico underscores the deliberate movement of production capacity toward regional alternatives that offer lower geopolitical risk and shorter transit times to U.S. markets.

Supply Chain Resiliency

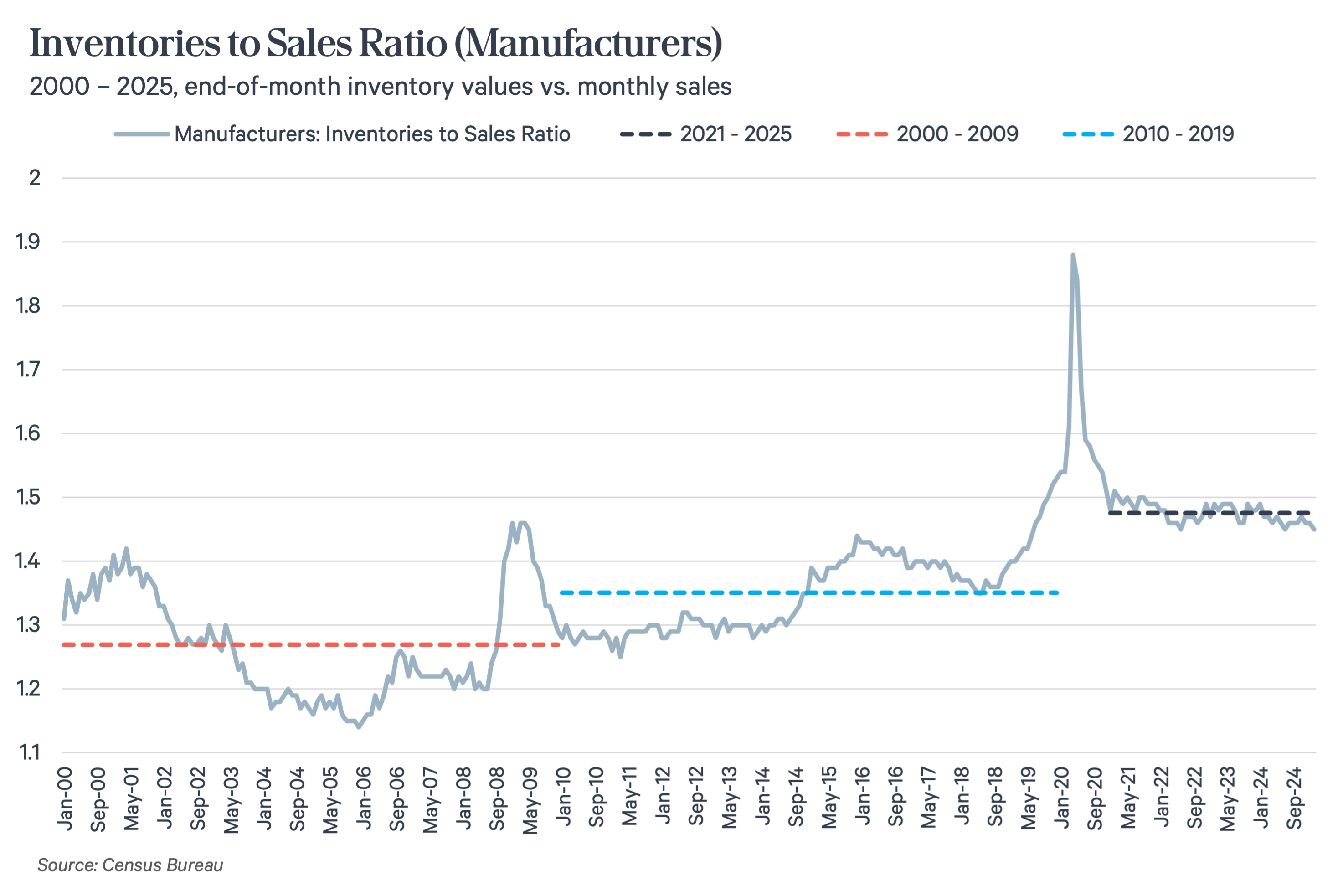

The Covid-19 pandemic exposed the vulnerabilities of ultra-lean, globally stretched supply chains. The pre-pandemic emphasis on capital efficiency has shifted towards risk mitigation and operational flexibility. We see this most clearly within the manufacturing sector where firms appear to be maintaining higher inventories as a hedge against future disruption. Higher inventories at the production level should translate into greater and more consistent demand for warehousing capacity, particularly in locations tied to manufacturing, regional distribution, and modal flexibility (i.e., the ability to shift between truck, rail, and air freight). We expect that the current trade turbulence will encourage companies to further embed resiliency into supply chain strategies such that inventory buffering remains a structural feature of how goods move through the economy.

Advanced Manufacturing

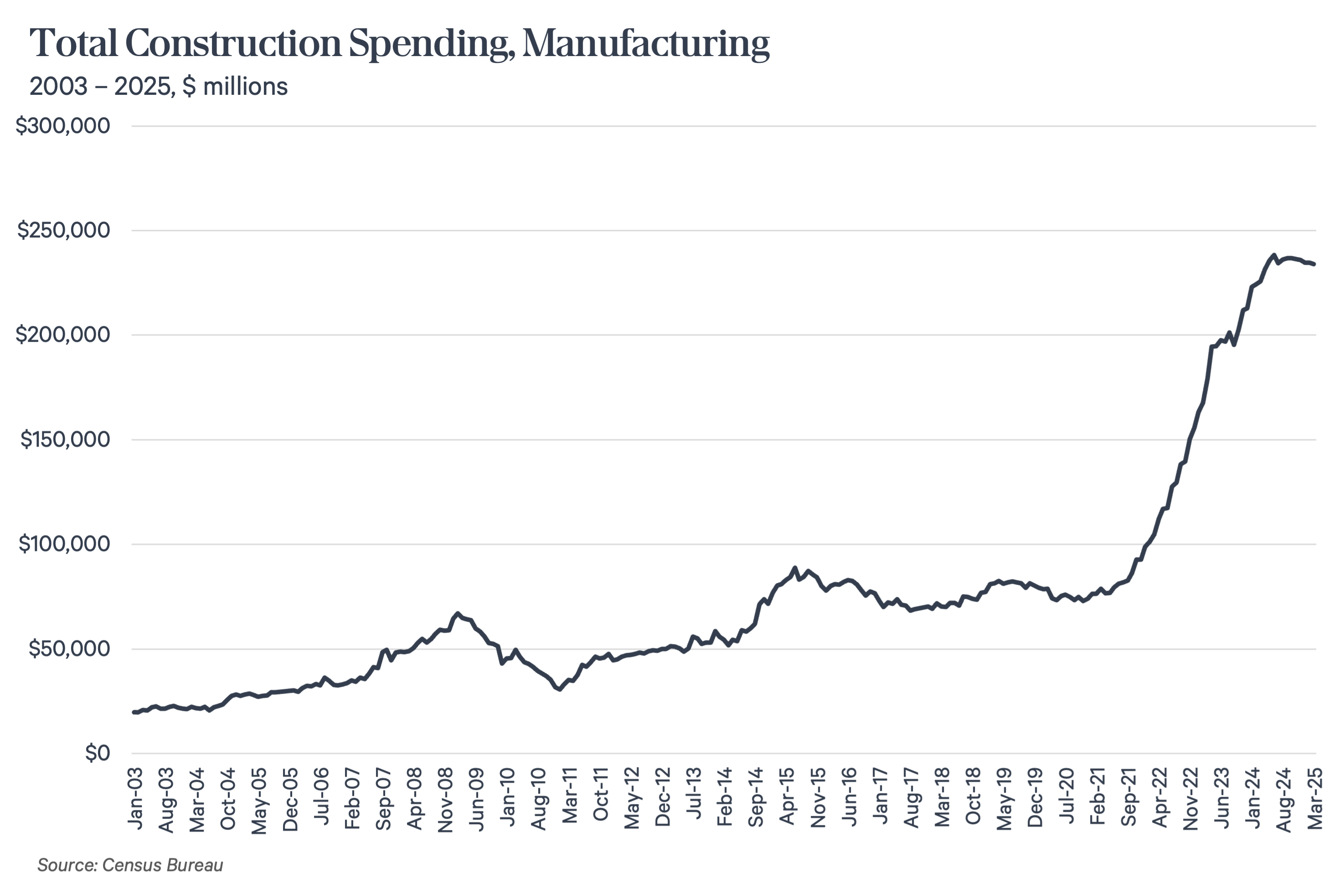

U.S. policy initiatives over the past several years–from the CHIPS and Science Act to the Inflation Reduction Act–have explicitly targeted the reshoring and expansion of high-value, technologically sophisticated production, generally referred to as advanced manufacturing. Construction spending on U.S. manufacturing facilities has surged dramatically since 2021 reflecting a wave of investment in semiconductors, electric vehicles, battery plants, and renewable energy components that has defined this new era of industrial policy. Advanced manufacturing requires highly coordinated supply chains, specialized inputs, and rapid distribution of finished goods. These demands create localized logistics opportunities–not only for raw materials and components flowing into production facilities, but also for regional distribution centers that serve end markets across surrounding population centers. Growth in advanced manufacturing is expanding the geographic footprint of logistics demand while at the same time reshaping the U.S. industrial base.

Dual-Demand Engine

These long-term structural forces—nearshoring, supply chain resiliency, and advanced manufacturing—were underway well before the current trade turbulence. Today, they are increasingly driving U.S. industrial real estate through a dual-demand engine. On one side, inventory buffering, regional distribution, and modal flexibility continue to support logistics demand tied to broader supply chain distribution. On the other, advanced manufacturing sectors—including semiconductors, EVs, and clean energy—are generating growing demand for manufacturing-adjacent logistics. Together, these forces are expanding the need for both regional distribution capacity and facilities positioned near critical production hubs. While the current trade conflict has sharpened focus on these issues, its role is secondary. These demand drivers are either accelerating as a result of trade volatility or unfolding independently of it.

Framework for Long-Term Supply Chain Evolution

Against this backdrop, we are working from five key assumptions that we expect to shape the long-term evolution of global supply chains. While not definitive forecasts, they reflect a framework for how companies are likely to balance efficiency, resilience, and proximity in the years ahead—and, in turn, where future logistics demand will concentrate.

| Assumptions | Logistics Real Estate Implications | Geographic Implications |

| Supply chains will become more geographically redundant | More distributed supply chains require additional logistics infrastructure across multiple nodes–not just in major coastal and inland hubs. | Proximate secondary nodes and intermodal corridors that provide alternative pathways into major consumption centers (e.g., Stockton, CA, Gainesville, GA). |

| Inventory strategies will remain structurally higher | Higher baseline inventories translate into sustained need for bulk storage and regional distribution centers. | Major consumption markets (e.g., Atlanta, Dallas-Fort Worth, Chicago), import-driven hubs (Southern California, Savannah), and regional distribution centers positioned to serve population dense areas (e.g., Pennsylvania’s I-78/I-81 corridor, Indianapolis, Memphis). |

| Regionalization will partially replace hyper-globalization | Supply chains are shifting toward regionally focused production ecosystems that reduce exposure to long-haul trade routes and bring sourcing closer to end markets. | U.S.-Mexico border markets (e.g., Laredo, El Paso), Southeast U.S. manufacturing and distribution markets (e.g., Atlanta, Nashville), and key rail/highway interchanges connecting regional production to national distribution (e.g., Kansas City, Dallas-Fort Worth). |

| National industrial policy will anchor new logistics nodes | Advanced manufacturing clusters create localized logistics demand adjacent to production facilities. | Semiconductor and EV corridors (e.g., Phoenix, Austin, Detroit), battery and clean energy clusters (e.g., Reno, Southeast U.S. auto corridor), and adjacent logistics markets that can serve inbound components and outbound finished goods. |

| Optionality will become a core location strategy | Locations that offer multiple routing and modal options–such as access to highways, rail, ports, cross-border gateways–will become more valuable as firms design networks that can adapt quickly to shifting conditions. | Major intermodal hubs (e.g., Chicago, Dallas-Fort Worth, Memphis), cross-border gateways (e.g., Laredo, El Paso), and flexible network pivots at regional chokepoints (e.g., Harrisburg/Central PA, Kansas City). |

Macro Forces to Micro Markets

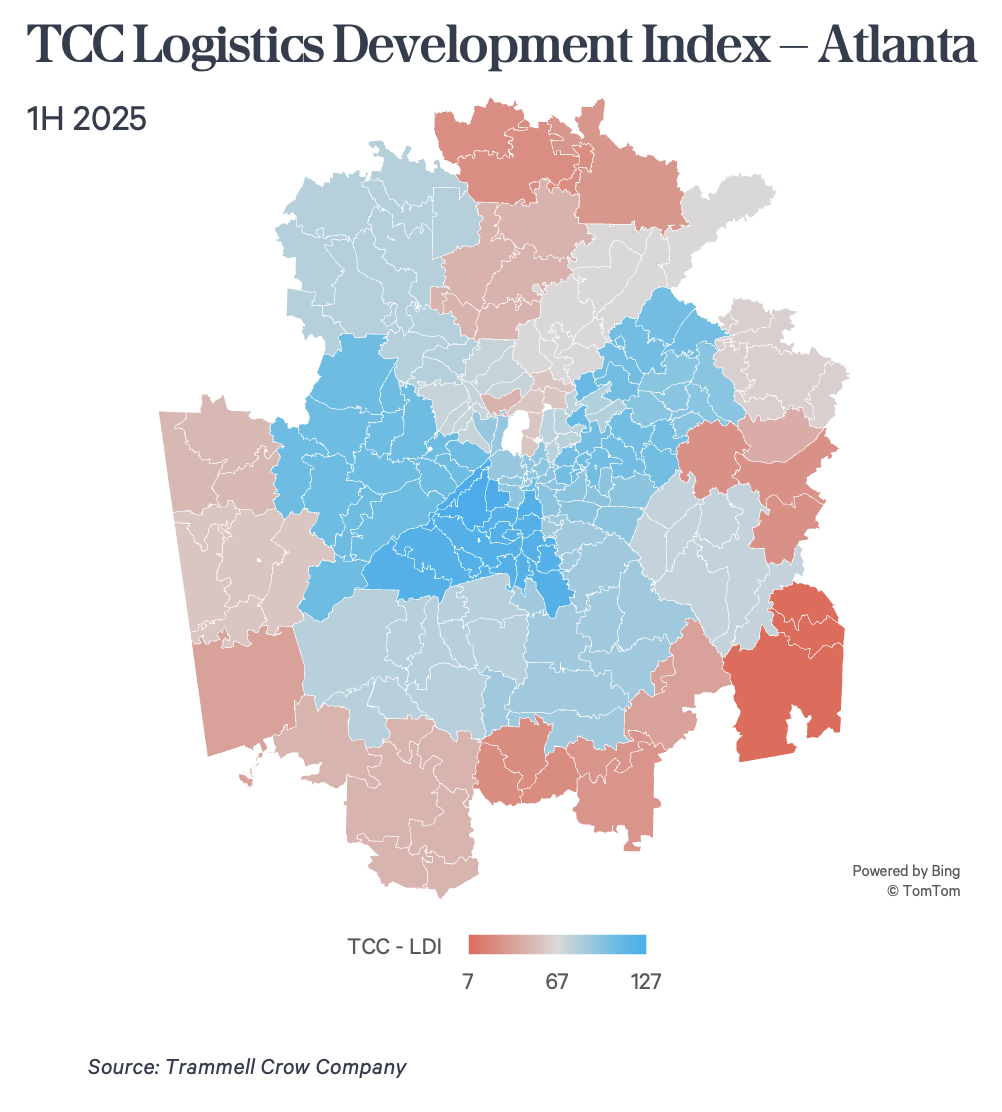

Supply chain diversification, manufacturing realignment, and regionalization are reshaping the demand map, but not evenly. Some markets–and, for that matter, submarkets–are poised to benefit far more than others based on their connectivity, cost structure, labor availability, and proximity to production and consumption nodes. This unevenness makes granular site selection essential. To that end, we developed our Logistics Development Index (LDI), a proprietary framework designed to evaluate and rank industrial submarkets based on their alignment with the structural themes outlined above. With novel ways of measuring supply chain drivers alongside broader market fundamentals like consumption trends, labor availability, supply characteristics, and performance forecasts, the LDI identifies locations where logistics demand is expected to be most resilient and sustainable over time. Crucially, this model is built up from the micro-market level to connect structural themes to the granular location decisions where development opportunities take shape.

Conclusion

The current trade conflict has heightened attention to supply chain realignment, but the long-term drivers of logistics demand remain rooted in structural shifts that began years ago. For industrial real estate, these shifts will sharpen distinctions across markets and submarkets, rewarding locations that align with new distribution patterns, manufacturing clusters, and diversified supply chains. Through the development of the Logistics Development Index (LDI), we have translated these complex themes into a framework that seeks to identify where structural demand and market fundamentals converge.